We've known for a while that tax changes are coming but have been waiting for specifics. While no legislation has been drafted, we recently got the high-level list of proposed changes in President Joe Biden's recently announced American Jobs Plan and the American Families Plan.

We do know that tax legislation has a fair chance of passing since Democrats plus independents control the House and have the needed 50 votes in the Senate plus a tie-breaking vote by Vice President Kamala Harris. Because of the need for 50 votes, an individual Senator can force changes by refusing to go along with a given provision. As a result, we expect that the current proposals, discussed below, will be tweaked by the drafting committees in the House and Senate.

One thing we know for sure is that taxes will go up although the Biden pledge is to not raise taxes on households earning $400,000 or less a year. It can't be emphasized strongly enough that now is the time to reach out to your wealth management team, CPA and estate planning attorney to discuss what you should be considering for both income tax and estate tax planning this year.

Retroactivity of new tax legislation

Will any changes be retroactive to Jan. 1, 2021 or instead take effect on Jan. 1, 2022 (or any date in between)? This won't be known until legislation is proposed. Comments out of the Biden Cabinet seem to be leaning towards an acknowledgment that it would be bad for economic recovery if the legislation was retroactive. There is also thinking out there that the changes to the capital gains rate could be effective prospectively on a date in the year 2021 announced by either the House Ways & Means committee by itself or in conjunction with the Senate Finance Committee, or such as the date of the initial draft of legislation.

Personal income taxes

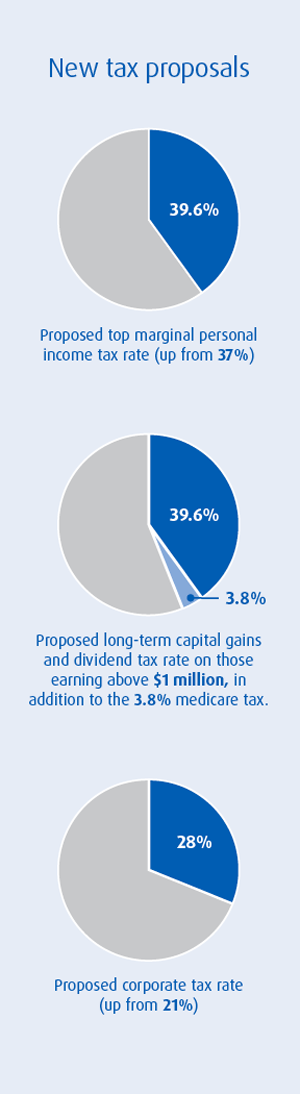

The American Family Plan proposes the following changes:

The American Family Plan proposes the following changes:

- Restoring the top marginal rate to 39.6% from today's 37% for households with incomes above $400,000.

- Raising the tax on long-term capital gains and dividends on those earning above $1 million to the ordinary income tax rate of 39.6%, in addition to the 3.8% Medicare investment income tax. As a result, for those earning above $1 million total tax on capital gains for Illinois residents will be 48.4%, California residents will be 56.7%, and residents in states with no income tax such as Florida and Texas will be 43.4%. However, it is speculated that the final new capital gains rate for these $1 million households will be something less than 39.6%.

- Taxing carried interests (private equity and hedge funds) as ordinary income instead of capital gains rates.

- Repealing Section 1031 like-kind exchange rules for real estate for gains on the sale of real estate in excess of $500,000.

- Imposing the 3.8% Medicare Investment Income Tax on active income from partnerships and S corporations for owners making more than $400,000 a year.

Note: Nothing was contained in the plans about changing the $10,000 cap on the state and local income tax deduction but it is still possible some change may appear once legislation is drafted.

Individual income tax strategies to consider implementing this year

- Sell appreciated capital assets sooner rather than later. If you had intended to sell appreciated capital assets in the relative near future, you may want to consider doing so in 2021 to take advantage of potentially lower capital gains rates. This has to be balanced against the effective date of this change and the possibility of retroactive tax legislation.

- Carried interests. See if you have the opportunity to cash out on any carried interest positions before ordinary tax rates kick in.

- Repositioning investment real estate. If you have been thinking about selling a property and purchasing a replacement property under the tax-deferral rules of Section 1031, you might want to accelerate those plans, assuming this new provision is not retroactive.

- Future investment real estate sales. If you have gains of more than $500,000 and you want to try to still take advantage of the Section 1031 deferral, you may want to see whether splitting up the ownership interests significantly in advance of the sale among your children would give you enough “bodies” ($500,000 per person) to keep each person's gain to the max of $500,000. You would be using part of your estate and gift tax exemption to do this. Keep in mind this would mean that the children would actually own part of any property acquired with the sales proceeds from the old property.

- Starting a new business. If you have set up a business as a C corporation in recent years, or anticipate setting up a new one, talk to your CPA about whether your investment can qualify as Section 1202 Qualified Small Business stock. If it does and you do business as a C corporation and hold the stock for at least 5 years, the first $10 million of capital gains (or 10 times your investment, whichever is greater) is exempt from federal income tax (but not state tax) when you sell if it is a stock sale; asset sales do not qualify. This break is limited to companies with $50 million or less of gross assets prior to your acquisition of the stock.

- Maximize contributions to retirement accounts and Roth conversions. Make sure to fully fund all retirement plans, and IRAs where applicable. Evaluate whether it makes more sense to fund a Roth 401(k) or Roth IRA going forward in order to get tax free income when you take distributions in the future. If you are planning on converting part or all of your existing retirement accounts to a Roth, it might make sense to do so at today's lower tax rate. In addition, you need to consider what your retirement tax bracket will be before deciding on a Roth conversion.

- Other retirement planning assets. Look at tax-deferred sources of retirement income such as life insurance with aggressive cash value build-up or annuities.

Corporate strategies to consider implementing this year

The Biden proposal is to raise the corporate tax rate to 28% (up from the current 21%) as well as to impose two minimum taxes: a 15% minimum tax on companies with book income over $100 million and a 21% minimum tax on foreign profits.

- Sell the company? Tax changes alone would not be a reason to sell your company. But if you are considering selling in the next few years you should evaluate whether it would be better to sell this year and take advantage of the 20% Federal Capital Gains rate (plus the 3.8% Medicare Investment Income tax plus your local state income tax).

- Dividend recapitalization. If your company can support the debt, now may be a time to pay dividends at the current 20% rate before it goes up next year.

- Shift income and expenses. Moving income you might earn in 2022 into 2021 could help you reduce the total taxes you end up paying. Business owners may have some leeway in when they choose to claim income and it might be worthwhile to think through how to do this now. By the same token, consider shifting expenses for which you will receive a tax deduction into 2022, when they can help you lower your taxable income in a higher tax year.

- Revisit optimum business structure. Now is a good time to meet with your tax advisors and discuss if you have the optimum business structure, whether it is a C corporation, S Corporation, partnership or LLC.

Dave Bensema, CPA, CFP® is a Managing Director with BMO Family Office, an integrated wealth management provider that serves ultra-affluent individuals, families and family offices across their tax, estate, investment, philanthropic, risk and family capital needs. Dave provides customized financial planning solutions to individuals and families as part of an overall personal wealth management strategy. He joined the organization in 1991 and has over 27 years of experience in the financial services industry. Jayne Hartley is a Regional Leader of Wealth Planning for BMO Wealth Management where she oversees the strategic development and delivery of customized wealth planning services to clients throughout the United States. Jayne is also a key member of the BMO's Business Owner Strategies and Solutions team, a specialized group of professionals that provides sophisticated wealth transfer, estate planning guidance to business owners and corporate executives. She has over 25 years of wealth planning experience. Pratik Patel is a Managing Director and Head of the Family Wealth Strategies team with BMO Family Office, an integrated wealth management provider that serves ultra-affluent individuals, families and family offices across their tax, estate, investment, philanthropic, risk and family capital needs. Pratik oversees the delivery of integrated wealth management advice and client service for ultra-affluent clients. His expertise includes financial planning, tax planning, wealth transfer planning, charitable and philanthropic planning, family governance and education planning and business owner and corporate executive planning.

“BMO Family Office” and “BMO Wealth Management” are brand names used by BMO Family Office, LLC, and certain affiliates providing investment, investment advisory, trust, banking, and securities products and services. These entities are all affiliates and owned by BMO Financial Corp., a wholly-owned subsidiary of the Bank of Montreal (“BMO”). Investment products are: NOT FDIC INSURED – NOT BANK GUARANTEED – NOT A DEPOSIT – MAY LOSE VALUE.